Digital transformation in banking isn’t just about implementing new technology—it’s about reinventing the way financial institutions operate to meet modern customer demands.

Transitioning from legacy systems to a digital core banking solution can propel banks into a future of agility, innovation, and efficiency. In today’s post, we explore key strategies for a successful transformation.

Start Small with an MVP Approach

Launching a digital core banking solution might seem daunting, but beginning with a Minimum Viable Product (MVP) can pave the way for a smooth transition. By focusing on core functionalities initially, banks can:

Accelerate Time to Market: Roll out essential features quickly and gather real-world feedback.

Mitigate Risk: Test new concepts on a smaller scale, ensuring that only the most valuable innovations are expanded.

Foster Innovation: Encourage continuous improvement and flexibility as the system evolves.

Starting with an MVP not only minimizes upfront risks but also builds a solid foundation for future enhancements.

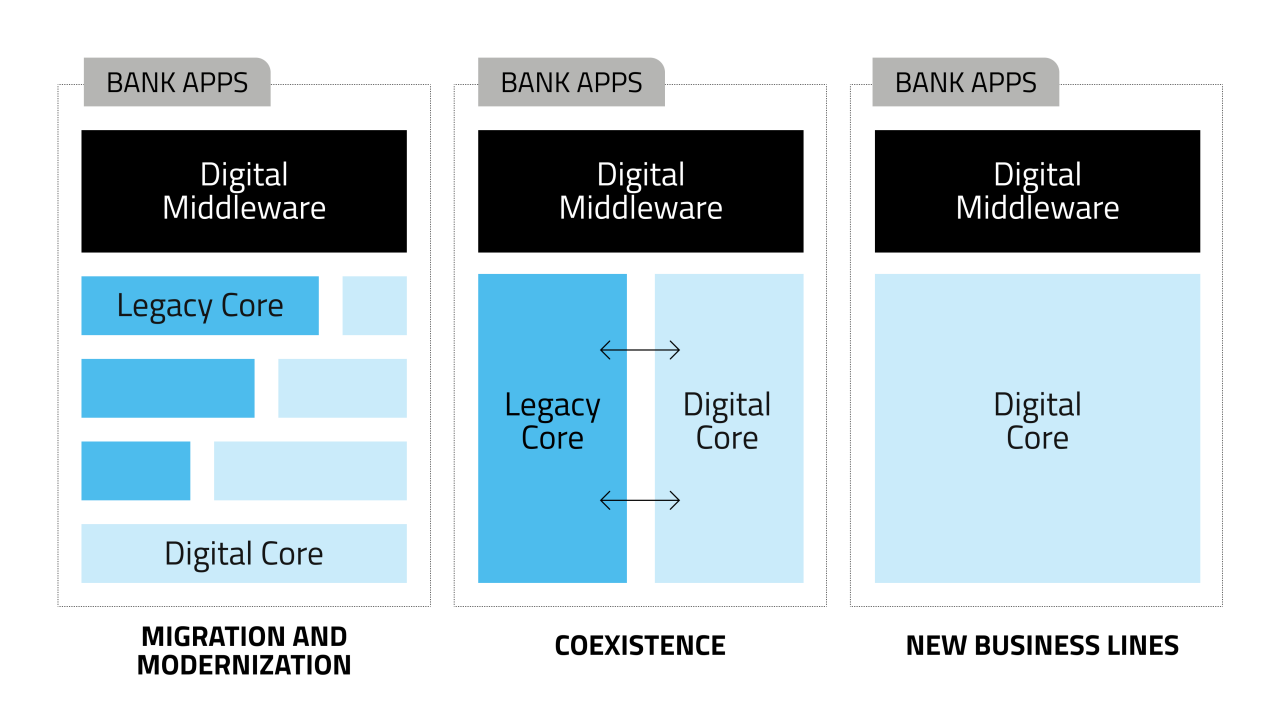

Dual-Core Strategy: Innovate While Maintaining Stability

A complete system overhaul isn’t always necessary. Consider a dual-core strategy where you:

Launch New Products on the Digital Core: Leverage the benefits of modern technology to offer innovative products and services.

Gradually Phase Out Legacy Systems: Allow existing products to continue running on the legacy core until they can be migrated or retired seamlessly.

This coexistence or New Business Line strategy ensures that innovation doesn’t come at the cost of operational stability, providing a controlled environment for transformation, always with a Digital Middleware decoupling the potential complexity we have in our backends to the rest of the organization and our customers.

Build on a Composable Architecture

A composable architecture is key to long-term success. This design approach involves developing a modular system where components can be easily added, updated, or replaced. Benefits include:

Flexibility: Quickly adapt to market changes or integrate new technologies without a complete overhaul.

Scalability: Efficiently scale the system to manage increasing transaction volumes and customer demands.

Simplified Maintenance: Update individual components independently, reducing downtime and operational costs.

Starting with a composable architecture means that your digital core can evolve alongside your business needs, ensuring both functional and non-functional scalability.

Coordinate Migration Strategies with Core Vendors

Migrating from a legacy system to a digital core requires careful planning and close collaboration with core vendors. Treat the migration as a dedicated project by:

Establishing a Strategic Partnership: Work hand-in-hand with your core vendor to design a migration plan that aligns with your business objectives.

Minimizing Disruption: Simplify migration steps wherever possible to ensure a smooth transition with minimal impact on day-to-day operations.

Implementing Dedicated Project Management: Set clear timelines, milestones, and contingency plans to tackle challenges as they arise.

A well-coordinated migration strategy ensures that the new digital core integrates seamlessly into your existing business ecosystem, reducing risks and paving the way for sustained growth.

Your Future, Your Move: Embrace the Digital Core Revolution

Adopting a digital core banking system is a transformative journey that goes beyond technology—it’s a strategic shift in how banks operate and deliver value. By starting with an MVP, leveraging a dual-core strategy, building on a composable architecture, and coordinating closely with core vendors, banks can navigate the complexities of digital transformation with confidence.

Embrace these strategies to not only modernize your core banking operations but also to unlock new opportunities for innovation, agility, and long-term success in today’s fast-paced digital era.